This blog post has been researched, edited, and approved by John Hanning and Brian Wages. Join our newsletter below.

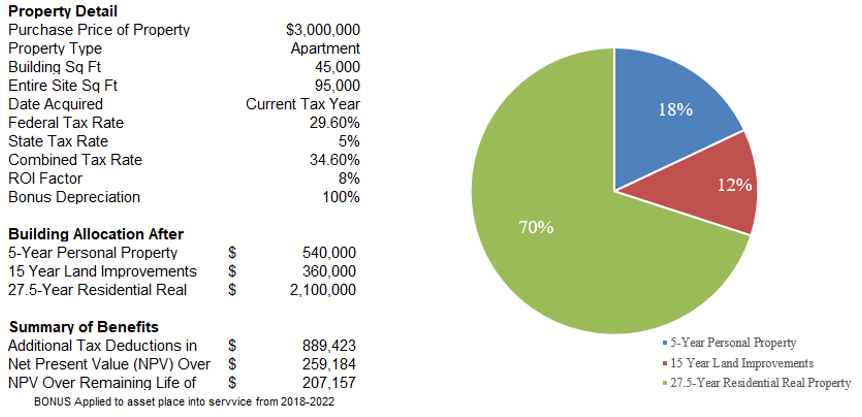

What is Cost Segregation?

Cost Segregation is a valuable strategy to increase cash flow and reduce income taxes for commercial property owners. The tax benefits of cost segregation can be applied to various types of real estate: apartments, assisted living/nursing homes, auto dealerships, office buildings, restaurants, manufacturing, hotels, medical buildings, retail space and others. The process of Cost Segregation segregating 1245 personal property components 1250 land improvements from the real property of a building, resulting in depreciable lives of 5, 7 and 15 years using accelerated depreciation

Beyond accelerated deductions the Tangible Property Regulations (TPR) allow taxpayers to write off disposed building components as a partial disposition. A cost segregation carves out building components so that a taxpayer can easily identify the deductible cost after a renovation.

Types of Transactions

- New Construction

- Property Acquisition

- Renovations or Expansion

- Leasehold Improvements

- Real Property Step-Up

For more information about our Cost Segregation services:

2024 Tax Guide